Tax MYTHtakes: TFSA, RRSP, or FHSA?

Photo Credit: Investopedia

By: Ken Lee, PFA | KLee Tax and Financial Services Co.

Published: 15 June 2026 4:00AM EST

Author's Note:

The Canadian Investment Regulatory Organization (CIRO) reports that a little more than 1 in 5 Canadians use and trust finfluencers (or financial influencers) on social media for financial advice. A great deal of these individuals have no formal training and lack any financial planning credentials. As a result, many, albeit not all, statements put forth by these individuals tend to be misleading or downright false. Over the next few articles of Tax MYTHtakes, I look forward to providing the truth to combat several myths commonly perpetuated by such finfluencers.

Yours,

Ken Lee, PFA

Disclosures: I am a PFA in good standing with Advocis and the Institute. This article is written purely for informative purposes. The views expressed are my own and do not represent those of any organizations I am affiliated with. The following should not be construed as legal nor tax advice. Consultation with your usual tax/legal professional is advised. Please contact us to discuss the contents of the article herein.

All references to a spouse include common-law partners. All references to the ‘Act’ or the 'ITA' mean the Income Tax Act, RSC 1985, c. 1 (5th Supp.), as amended.

Good morning, Toronto! Many finfluencers on social media claim, to varying degrees of truth, that Canadians coming of age NEED to immediately open several tax-advantaged accounts, including a Tax Free Savings Account (TFSA), Registered Retirement Savings Plan (RRSP), and First Home Savings Account (FHSA). One such short-form video on Instagram suggests that new adults should open an FHSA account ahead of a TFSA. In today’s article, we will discuss the basic design of these three plans, in addition to discussing several considerations that are often missed by these finfluencers.

An individual must be a Canadian resident and above the age of majority in their province (18 in Ontario) to open a TFSA or FHSA account. These registered accounts can hold a variety of different common investments in accordance with the investor’s risk tolerance and goals.

A TFSA allows individuals to shield their contributions and investment growth on a tax-free basis for perpetuity. Funds can be withdrawn on a totally tax-exempt basis at any time, for any reason, without affecting any income-tested government benefits (i.e. Old Age Security). For this reason, a TFSA can be a valuable tool to both supplement retirement income and also for everyday goals.

Example 1

Annika opens a TFSA on her 18th birthday and contributes the maximum of $7k. After some lucky purchases in AI stocks, her TFSA is now worth $167k on her 40th birthday.

- As all gains in a TFSA are sheltered from tax, Annika can withdraw all $167k without incurring any taxes.

An RRSP, in contrast, operates on a tax-deferred (delayed) basis. Contributions to an RRSP are deductible against taxable income, which allows taxpayers to reduce their present tax liability. Taxpayers may elect to defer the deduction and claim it in a future tax year. Deductions are of more value when a taxpayer’s taxable income and marginal income tax are higher. RRSPs can be an advantageous tax planning tool where there is a significant difference between a taxpayer’s marginal tax rate during their working years and their retirement years. Where ideally used, the taxpayer receives a deduction at a higher tax rate and withdraws at a lower rate.

Example 2

Artin and Hilary both contribute $10k to their RRSP. Their total taxable income for 2025 is $50k and $300k, respectively.

- Artin’s RRSP deduction results in $2,605 tax savings.

- Hilary’s RRSP deduction results in $5,353 tax savings.

- Hilary’s income put her in the top tax bracket of 53.53%, while Artin’s income put him in one of the lowest brackets of 19.55%.

- In the future, Artin should defer his deduction to when he was in a higher tax bracket.

Finally, FHSAs combine the best attributes of both TFSA and RRSPs. FHSAs allow taxpayers to deduct from their income any contributions made towards the account, like RRSPs. Deductions can be carried forward indefinitely, even after the account is closed. As with TFSAs, investments can grow on a tax-free basis. However, the funds have a specified purpose: they are to be withdrawn only to buy a first home. If the funds are not used for this purpose, the account will be closed by 31 December of the year following the 15th anniversary of opening the account. At such time, the entire value of the FHSA can be rolled over into an RRSP. An unused and closed FHSA is functionally the same as an RRSP from a tax perspective.

Example 3

Richard opened an FHSA on 15 June 2025. He proceeds to contribute the maximum of $8k. He makes no further contributions. On 15 October 2030, he withdrew the full value of the FHSA, which has now grown to $10k, to purchase a home.

- The FHSA plan must be terminated by 31 December of the year following his withdrawal (31 December 2031)

- Richard may choose to deduct $8k from his income for the 2026 tax year, or carry forward to a future tax year.

- His $10k withdrawal is tax-exempt.

Example 4

Benjamin opened an FHSA on 15 June 2025. Over the next 5 years, he contributed the maximum of $40k. It is now 2041.

- The FHSA plan must be terminated by 31 December of the year following the 15th anniversary of the plan (31 December 2041)

- If, by 31 December 2041, Benjamin does not make a qualifying withdrawal, the FHSA funds will be diverted to his RRSP. The tax-exempt nature of the account will be downgraded to that of a tax-deferred nature.

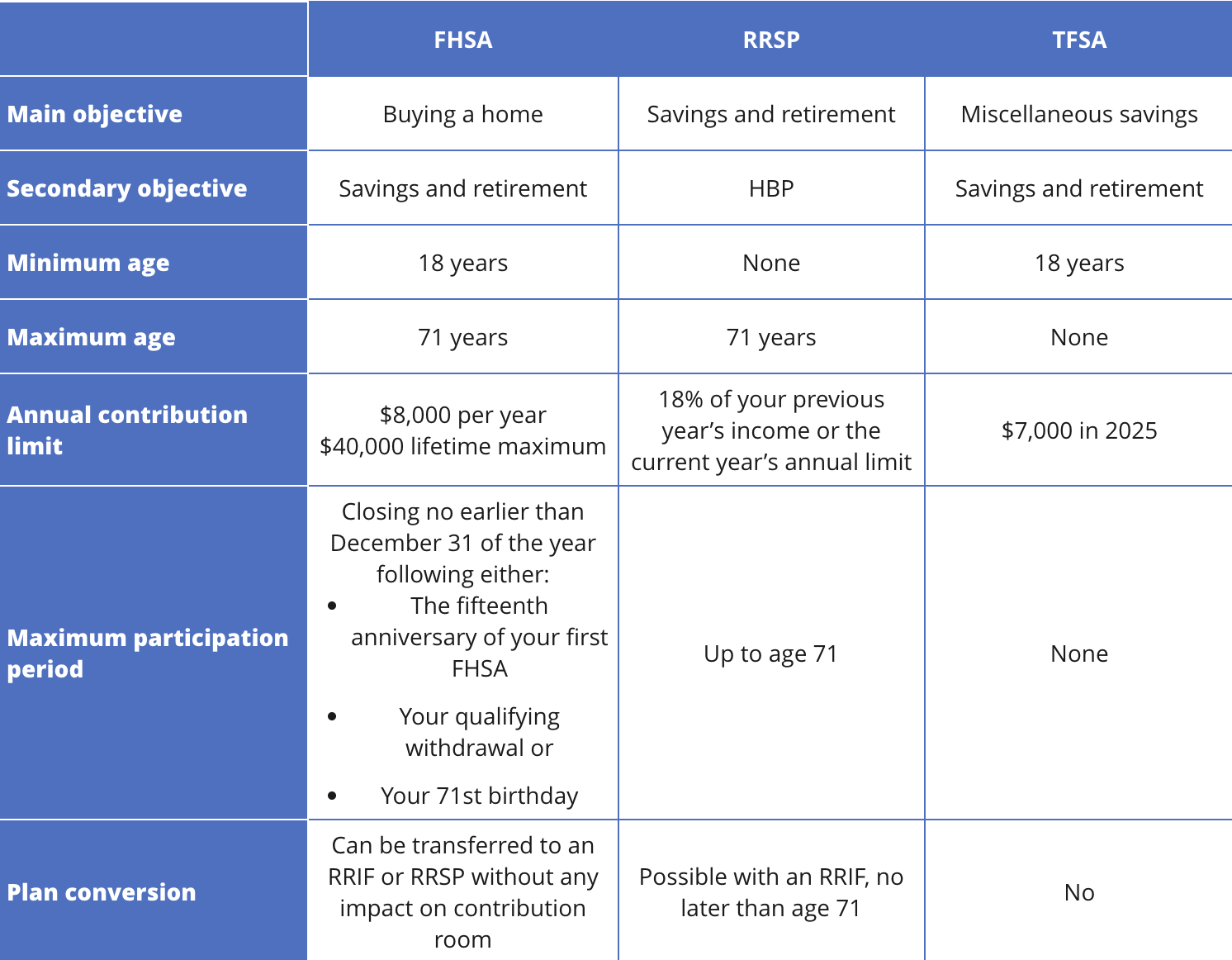

The differences between these three accounts can be summarized by the following table:

Figure 1: TFSA/RRSP/FHSA Comparison Table (Credit: iA Financial Group)

Teenagers may have some RRSP contribution room as a result of having a part-time job. However, this room may be eroded by pensions and retirement savings plans that employers may offer. Generally, funds permitting, new adults tend to feel faced with the choice of contributing EITHER to a TFSA and/or FHSA. While many videos and even professionals strive to rank either one above the other, in reality, I argue that this choice is much more nuanced. Such a determination is dependent on the investment goals of each individual — an individual who does not foresee buying a house within 15 years should not open a FHSA.

Dangerously, many finfluencers fail to inform their viewers of situations in which tax-advantaged accounts may be subject to immediate tax. For example, while a TFSA is indeed exempt from Canadian tax, certain foreign taxes can and do apply to investments held. Many Canadians invest in US securities, and it is not unusual for a TFSA portfolio to comprise shares of American companies on American stock exchanges. When a US-based corporation pays dividends to a Canadian resident investor, Article X of the Canada–United States Income Tax Convention (the 'Treaty) provides that 15% of the dividend is withheld as tax. Such withholding is reduced to 0% if the stocks were instad held in an RRSP, due to an exception within the Treaty. While out of the scope of this article, differing tax treatments across securities naturally lead to another area of tax planning: asset location.

Example 5

Corwin owns $10,000 worth of CAD-hedged Apple Inc. stock that listed on the TSX in both his TFSA and RRSP. In 2025, Apple’s dividend yield was 5%.

- Despite Apple’s stock being listed on a Canadian stock exchange, it is still a US-situs company. Thus, Article 10 of the Treaty applies.

- There would be 15% withholding on dividends within the TFSA and 0% withholding for the RRSP.

- Corwin would ultimately receive $425 and $500 of dividends from the stock within his TFSA and RRSP, respectively.

Many Canadians are similarly uninformed of the ramifications of ceasing to be a Canadian resident on their tax-advantaged accounts. While many seem to believe that their accounts retain their tax-advantaged status worldwide, this is untrue. The new jurisdiction will generally apply its own rules to worldwide income and foreign accounts, which can be treated as fully taxable accounts.

No better example can be seen than with Canadians who become US residents, or are already US residents (such as by virtue of being a US citizen). The Internal Revenue Code (IRC) and Treaty do NOT recognize the tax-exempt status of TFSAs, although RRSPs retain their tax-deferred status. As such, should dividends or a capital gains event occur within a TFSA, the US will fully tax the gains, even if Canada does not impose any tax.

In addition, due to the onerous compliance regime characteristic of the US tax system, the taxpayer would likely have to include their TFSAs and RRSPs on their annual Report of Foreign Bank and Financial Accounts (FBAR) filings. In addition, Mutual Funds (MFs) and exchange-traded funds (ETFs) are popular means of diversifying investments in Canada. MFs and ETFs generally meet the Passive Foreign Investment Company (PFIC) tests of IRC §1297. Canadians holding investments that are classified as PFICs are required to file Form 8621. Worse, the US imposes the highest marginal tax bracket on PFIC gains.

Example 6

Sophie, a Canadian-American dual citizen, owns $25k of the ETF “K.TAX” in her TFSA. The ETF is a PFIC within the meaning of IRC §1297.

- Sophie is a Canadian and American tax resident.

- Sophie must file an FBAR and list all foreign accounts owned due to the TFSA exceeding the filing threshold.

- She must file Form 8621 as a result of the ETF being a PFIC.

- Any event in the TFSA would be fully taxed in the US.

- Sophie would be unable to deduct any Foreign Tax Credits on her potential US tax liability, due to having paid no tax in Canada with respect to her TFSA.

In conclusion, while it is indeed important for young Canadians to open tax-advantaged accounts, it is equally important to consider investment objectives and future goals when choosing where to allocate funds. Financial professionals have an obligation to perform thorough due diligence on a client’s financial background to best inform their recommendations. Finfluencers have no such obligation — it is impossible to offer perfectly personalized advice to mass audiences. Unfortunately, people can and do suffer adverse tax consequences as a result of overly relying on such individuals.

--------

Too complicated? No worries! We file tax returns and offer tax planning services to individuals and not-for-profit organizations. Whether you are working your first job or an NPO looking to make a difference, you can be sure that KLee Tax will be there for your tax needs, when and where you need us.

Contact us below for a consultation or to discuss the contents of this article!